Since the government introduced auto enrolment back in 2012, more than 10.5 million people in the UK are now enrolled in a workplace pension(1), helping to address the lack of pension savings among a large number of the population. It’s brought 4 million first-time savers and 5 million people who earn less than £20,000 a year into pension saving.

And while it’s fair to say that auto enrolment has been a success, the growth of these workplace pensions has spawned another, equally pressing, problem – that of ‘small pension pots’.

Many of the employees enrolled in these schemes have worked in several jobs since 2012, building up small amounts of pension savings across different schemes with different employers. Yet very few of them do anything other than ignore the pension they left behind. In fact 98% simply leave that pot where it is, sitting untouched.

An average of 11 jobs over a lifetime

The problem of these ‘small pots’ is only going to continue to grow, primarily because of high job turnover. Data from the Department of Work and Pensions shows that the average person now has eleven different jobs over their lifetime, and one in four of us will have sixteen or more employers. (2)

We asked the Pensions Policy Institute (PPI) to analyse the scale of the problem, and their researchers estimated that there’ll be 27 million small pension pots in existence by 2035.

Lose-lose situation for members and providers

The end result is that members of these schemes face paying management charges for each pot and watching their hard-earned savings gradually being eaten away by those charges, while auto enrolment pension providers accrue duplicate administrative costs. This isn’t fair for either members or providers.

So what’s the plan?

To tackle this, the government is introducing legislation, due in April 2022, to prevent pension providers from collecting charges from any individuals who have savings worth less than £100 in a single pot, which is good news.

This is important because three quarters of deferred pots contain pension savings of less than £1,000 and 25% contain less than £100. But please don’t dismiss these pots as trivial. Out of every single acorn, mighty oak trees grow, and every pound saved towards retirement is important.

But the pressing need is to tackle the wastage that multiple pots cause through duplication of administration and help members maximise the value of all their pension savings. It’s like leaving the lightbulbs on in all the rooms of your house. Far better to consolidate, so that members can quickly and easily move their savings into a single (and growing) pot each time they move jobs.

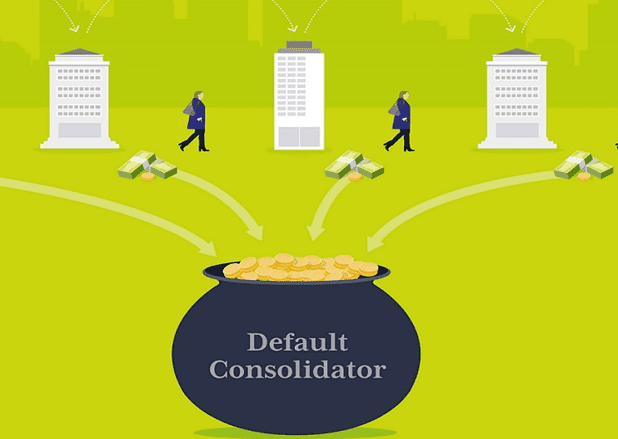

Step up the default consolidator

There’s been several solutions tabled to tackle this problem. But our view is that the simple – albeit unimaginatively named – ‘default consolidator’ meets the needs of both members and auto enrolment providers. Each time an employee leaves a job, their workplace pension savings in that scheme automatically transfer to their default consolidator.

This is a high-quality pension scheme which specialises in accepting transfers over an employee’s working lifetime, helping to build up their pension savings and ensure they only pay a single set of charges on the funds in their consolidator.

And a single, consolidated pot is simpler and more cost-effective for providers to run.

How would it work?

Like all the auto enrolment master trust schemes, the different consolidators would be authorised by The Pensions Regulator (TPR) to ensure they’re run by fit and proper people, in members’ interests. Companies which operate consolidators will need to have efficient systems, a well thought-out investment strategy and be able to prove that they’re financially sustainable – like the current master trust regime.

Every time an employee leaves a job where they’re auto enrolled in a workplace pension, their pension will automatically transfer to their default consolidator.

Member’s choice to opt out and opt in

If they’ve left only a small pot behind, they’ll be given the opportunity to opt out of the process, otherwise money will be automatically transferred from their old employer’s scheme to their default consolidator.

But if they’ve left a larger pot behind, it’s reasonable to expect them to engage with their pension saving, so they’ll be told that their savings may be consolidated, but they must opt in to make it happen.

Choose and switch consolidators

It’s essential that members are able to choose their consolidator as well as switch their savings to another authorised consolidator at any time. TPR authorisation will give them the confidence to know that their choice is sound.

Members will also benefit from the fact that they’re:

- at less risk of losing old pension pots

- not paying multiple fees for duplicate administration services, and that

- there’s a consistent investment philosophy for all their consolidated savings.

This will enable them to steadily grow their savings over time, and hopefully engage more actively with pension saving during their working life, helping them to make better decisions at retirement.

Adrian Boulding, former policy director, NOW: Pensions

Sources:

(1). TPR monthly automatic enrolment declaration of compliance statistics

(2). DWP Making Automatic Enrolment Work Review

NP/B0022